IRC Conformity Summary - Update

From the House of Representatives - Representative John Carson,

Download Original Document

March 6, 2026

Fellow CPAs, Tax advisors,

As you are aware, the state of Georgia must pass an IRC conformity bill each legislative session, to specifically adopt or not adopt income tax provisions that have been changed by Congress during the prior calendar year. Although usually just an annual housekeeping measure, this year’s legislation has required much more analysis and revenue consideration than usual, due to the tax law changes from last year’s HR 1, the Big Beautiful Bill.

I’ve heard from many tax CPAs, noting that various tax software platforms (CCH, Lacerte, Intuit, etc.) are flagging various issues since Georgia has not finalized IRC conformity for 2025 tax year. I share this frustration and understand the delay this is causing to proper filing of GA 500s, GA 600s, and other returns.

Below is an overview of the bill’s status, frequently asked questions, etc.

Is there a delay with the IRC conformity bill?

Our IRC conformity bill, HB 1199, passed the Georgia House of Representatives on February 20th.

It subsequently passed the Senate Finance Committee on Wednesday, February 25th. I’m told that the Senate

Rules committee is implementing some changes to the current version of the bill.

Timing/What are the next steps?

As of the date of this letter, the Georgia Senate is expected to vote on HB 1199 sometime during the week of March 9th. From there, assuming any changes are agreed upon, it will be sent back to us in the Georgia House for an Agree motion and then immediately to the Governor’s desk.

I’m also told that tax software platforms, such as the ones noted above, will be made aware of our IRC conformity upon final passage.

Will Georgia adopt a $40,000 SALT deduction, as done in HR 1, the Big Beautiful Bill?

No. In our IRC conformity bill from calendar year 2018 (which addressed many of the federal tax provisions

changes in the Tax Cuts and Jobs Act from 2017), Georgia adopted the following language:

OCGA 48-7-27. Computation of taxable net income:

(b)(3) There shall be added to taxable income any amount deducted pursuant to Section 164 of the Internal Revenue Code in determining federal taxable income that exceeds the following:

o (A) For a single taxpayer, a taxpayer filing as head-of-household, or a married taxpayer filing jointly, $10,000.00; or

o (B) For a married taxpayer filing separately, $5,000.00.

We are not proposing any changes in HB 1199 to this section of our state revenue code.

Will Georgia exempt tips and overtime income, as done in HR 1?

Not for 2025 tax year.

If Georgia adopts any exclusion from AGI of either tips or overtime pay, this will be considered in separate

legislation. There are currently several proposals to adopt some state tax relief from tips and overtime,

including HB 1370.

As mentioned above, if Georgia does adopt any AGI exclusion of tips or overtime pay, it will almost certainly

not impact state tax year 2025, due to issues with proper reporting and administration.

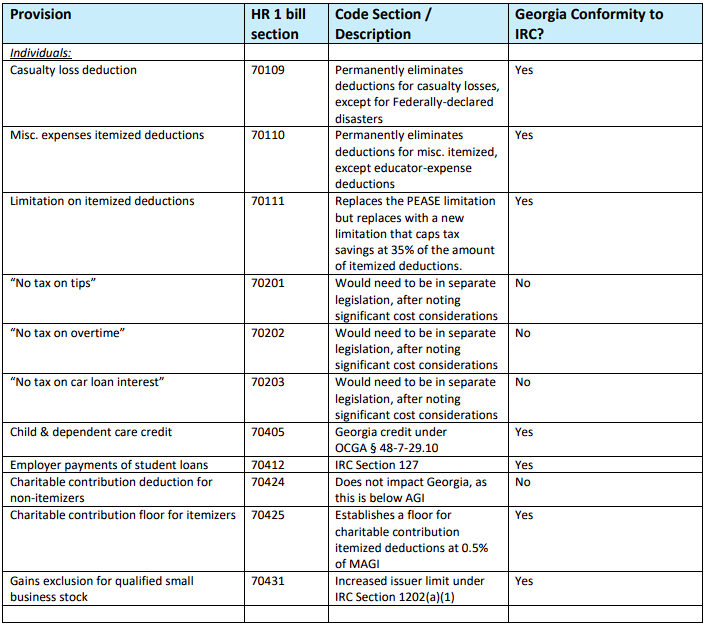

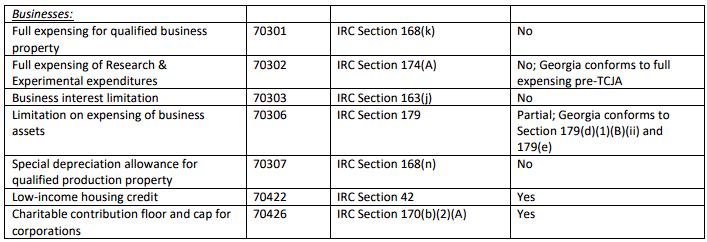

Overview of the proposed changes

As provided earlier, here is a brief summary of the proposed changes in the IRC Conformity bill:

I trust this update is helpful to you and your practice. Please feel free to reach out to me with any

questions.

Proud to represent our profession here at the State Capitol.

Sincerely,

Rep. John Carson, CPA

(R-NE Cobb, SE Cherokee)